Welcome to the FAQ section of the DRIVE Project Takaful! Here, we aim to provide you with comprehensive answers to common questions about our innovative initiative.

- What is Takaful?

- What is Sharia Compliance?

- What makes Takaful Sharia compliant?

- How does Takaful differ from insurance?

- Must surplus be paid to participants in a takaful contract?

- What is ReTakaful?

- How does index-based livestock Takaful (IBLT) work in practice?

- What Takaful model does the DRIVE product adopt?

- What is the status of the Takaful market in Somalia?

- Is the local Takaful market holding the risk under DRIVE?

- How is Sharia compliance established in Takaful?

- Why is there a need for a Supreme Sharia Supervisory Board (SSSB) or National Sharia Council?

What is Takaful?

Takaful is a mutual insurance concept that operates in accordance with Islamic principles, which are based on fairness, transparency, and social responsibility. It is designed to help people protect themselves against risks and losses, while remaining true to their religious values and principles.

What is Sharia Compliance?

Shariah compliance is the adherence to the Shariah rulings and principles found in the main sources of the Holy Qurán and the Prophetic traditions. The five overriding objectives of Shariah law can be summarized as safeguarding one’s Religion, Selves, Minds, Progeny and Wealth.

Such rulings can either be based on ijtihad, tawil, or qiyas. The bulk of Shariah rulings and principles are firm and intact over time and are unchangeable. However, the status of the compliance can change over time, depending on circumstances at the time of the ruling. This is particularly true of finance, e.g. both banking and insurance.

What makes Takaful Sharia compliant?

The key principles of Shariah compliance in the context of Takaful are:

- The prohibition of gharar, which refers to uncertainty or ambiguity. This means that Takaful is based on a contract of tabarru’ (donation) and not a contract of exchange like conventional insurance. According to Shariah, gharar, can affect contracts of exchange but not contracts of donations such as Takaful. Further, Takaful products must be designed in a way that is transparent, fair, and avoids ambiguity. The terms and conditions of the Takaful contract must be clearly defined, and the risks and benefits of the product must be clearly understood by the policyholder (termed ‘participant’ in Takaful).

- The prohibition of the practice of maysir, or gambling. This means that Takaful is a mechanism of risk sharing (akin to mutual insurance) rather than transferring risk. Participants contribute funds to a common Fund to protect against losses. These contributions are termed tabarru or donations. The takaful Fund is managed on behalf of the participants by a Takaful Operator in exchange for a fee (the wakala or agency fee). Participants of a Takaful scheme are considered co-owners of the Fund and share in the surpluses and deficits of the Fund. This approach encourages members to take an active role in managing risks and helps to create a sense of community and mutual support.

- The prohibition of riba, which refers to interest or usury. This means Takaful operators invest a portion of the Takaful Fund in Shariah-compliant investments only. Takaful Operators cannot invest in interest(riba)-based financial instruments, such as bonds or fixed deposits. Instead, Takaful Operators invest in Shariah-compliant assets, such as equities (of companies that exclusively engage in Shariah-compliant businesses), real estate, and other non-interest-based financial instruments.

- The prohibition of riba also means that if the takaful Fund falls into a deficit the Takaful Operator provides a qard (an interest-free loan), which would be a first charge on any future surpluses arising from the common Fund.

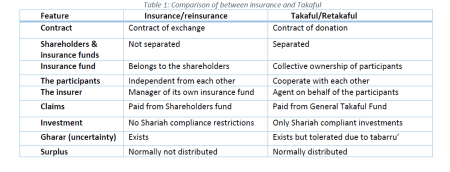

How does Takaful differ from insurance?

Takaful is a system whereby participants share risk by making specific contributions into a Fund that is used to pay for losses suffered by its members. Takaful is premised on mutual co-operation and solidarity, therefore entails risk sharing.

Insurance (other than mutual insurance) involves the transfer of risk from individuals to an insurance company in exchange for a specific premium payment. The insurance company takes on speculative risk wherein it expects that the total premiums it collects would exceed the sum of the expenses it incurs and total claims it pays out. This is akin to the practice of maysir, or gambling, which is forbidden under Shariah law. Takaful is a Shariah-compliant alternative to insurance.

Table 1 compares the key features of insurance and Takaful.

Must surplus be paid to participants in a takaful contract?

Payment of surplus to participants is not mandatory. The decision to pay surplus is based on actuarial assessment of the sustainability of the Takaful Fund. It is made when the total amount of the Fund is sufficient to cover losses in the foreseeable future.

What is ReTakaful?

Retakaful is a Shariah-compliant form of reinsurance. In contrast to reinsurance, where the insurer (to whom the risk has been transferred by the insured) offloads a portion of the risk to the reinsurer, the Takaful pool actively shares risks with the Retakaful pool. This sharing is facilitated through the payment of a contribution from the Takaful pool to the Retakaful pool.

The Retakful Operator takes a wakala fee from this Retakaful contribution in return for managing the Retakaful Fund. The Retakaful Operator meets its expenses of managing the Retakaful Fund from this fee. Similar to the Takaful Operator, the Retakaful Operator is obliged to make a qard payment to the Retakaful pool should a deficit arise. This is subsequently repaid from future surpluses from the Retakaful Fund.

How does index-based livestock Takaful (IBLT) work in practice?

IBLT is designed to prevent the loss of livestock due to drought by providing funds for pastoralists to purchase feed for their livestock when there is inadequate pasture. It is not meant for restocking after livestock loss.

The payout is based on an index that measures the level of pasture in an area. If the pasture available for livestock is too low (i.e. the vegetation index falls below a minimum level of greenness) the contract pays out a sum of money which is enough to keep a unit of livestock alive. The payout is therefore less than the total value of a livestock and is unlikely to cover the cost of replacing a lost livestock, illustrating the preventive intention of this intervention.

What Takaful model does the DRIVE product adopt?

Figure 1 summarizes how the Takaful scheme for pastoralists in Somalia operates based on a hybrid Wakalah and Mudarabah model. Total contributions from the Government and pastoralists are first split between a wakala fee and a tabarru’.

The Takaful Operator uses the wakala fee to cover its own expenses.

The General Takaful Fund pays a retakaful contribution into a General Retakaful Fund, which is to manage the risk of the General Takaful Fund being inadequate to cover all the members’ losses.

A portion of the General Takaful Fund is not used to pay claims but to invest in sharia-compliant investments, which increases the total amount of funds available in the General Takaful Fund to cover members’ losses. The Takaful Operator manages the investment on behalf of the participants. The proceeds from investments are shared equally by the Takaful Operator and the General Takaful Fund.

In the event of a loss by a participant, the Takaful Operator pays using money from the General Takaful Fund as well as from recoveries from the General Retakaful Fund.

If the total amount available in the General Takaful Fund and the General Retakaful Fund is not enough to cover the losses, the Takaful Operator provides an interest-free loan (Qard) to the General Takaful Fund. In the event of an annual surplus, the fund first pays back any outstanding Qard provided by the Takaful Operator, if applicable. Once the Qard is completely paid back, participants may receive a share of the remaining surplus.

Note: The General Takaful Funds in Somalia are not yet being used to pay losses because this is a new product and will require time for the Funds to accumulate sufficient capital and reserves. Takaful funds in Ethiopia cover 10% of the losses and the Retakaful and retrotakaful Funds cover the balance.

What is the status of the Takaful market in Somalia?

The Somalian market is nascent, comprising 6 Takaful Operators and 1 broker, each with two to nine years of existence. There is no Retakaful Operator. Between 2019 and 2022, total contributions increased by over 40% from US$6.5 million to US$9.2 million. However, the bulk is from medical cover for expatriates.

Is the local Takaful market holding the risk under DRIVE?

Given the nascent nature of the Takaful Operators in Somalia, their Takaful Funds are not being used to underwrite the losses (underwriting here refers to a source of qard to cover any excess of claims over contributions). Instead, the losses are being met from the Retakaful Funds of participating Retakaful Operators through ZEP-RE. In time, it is expected that local Takaful Operators will retain a portion of the risks in their respective takaful funds. This temporary arrangement has been considered shariah compliant on an exemption basis by the ZEP-RE sharia advisor.

The ZEP-RE Retakaful Fund in turn is not expected to retain all the risks and thus require (conventional) retrocession support as currently there is no capacity to retrocede to another retakaful fund. Again, this is considered as Shariah compliant by the ZEP-RE Shariah advisor on a temporary dispensation basis.

How is Sharia compliance established in Takaful?

A Takaful Operator establishes a Shariah Supervisory Board (SSB) to provide guidance and oversight to management to ensure that all Takaful operations are in line with the values and principles of Shariah. The SSB is made up of experts in Islamic law and finance.

The SSB is responsible for ensuring that the Takaful Operator manages the operations in an ethical and socially responsible manner. The SSB reviews the full range of operations including:

i. The design, operation, and management of Takaful products and services.

ii. All operations, including investments, contracts, risk management, and governance.

iii. The social and environmental impact of the Takaful Operator’s investments.

Why is there a need for a Supreme Sharia Supervisory Board (SSSB) or National Sharia Council?

In summary, while insurance is not Shariah compliant, Takaful is, based on the opinion of the appointed Shariah scholar. As the interpretation of Shariah law can vary even within a jurisdiction (depending on the teachings and understanding of the subject matter by the Shariah scholar involved) it is vital to have a common understanding of what is considered Shariah compliant and what is not within the regulated jurisdiction This would avoid confusion to the public and allows the regulator to issue takaful regulations that apply consistently across the industry. Thus, there is a need for a Supreme Sharia Supervisory Board (SSSB) at the regulator level whose fatwas (a ruling or point in Islamic law) are generally accepted by those governed by the laws of the country. The SSSB provides guidance and oversight by issuing operating standards and guidelines that ensure that all Takaful operations in the country are in compliance with Shariah principles as interpreted by the SSSB. By following these principles, Takaful operators can provide a socially responsible alternative to conventional insurance, while remaining true to their religious values and principles.